Ensure you modify the field above with your name and student number above immediately

The exam has XXXXX questions, each with multiple parts for a total of XXXXX points. You may not finish the exam, so best to do your best answering all questions to the extent possible and not get stuck on any one question.

This exam is closed book and accessing the internet is not permitted

See the formula “sheet” embedded at the end of this notebook for reference

You can the internal help as required (see the Jupyterhub menu, use Settings/Show Contextual Help)

Execute the file to begin, which will also check your setup. To do this in Jupyter, in the menu go > Run > Run All Cells or the equivalent buttons

Edit this file directly, and in-place as an ipynb file, which we will automatically download at the end of the exam time directly. In particular

DO NOT rename this file with your name. It is automatically associated with your canvas account

DO NOT save-as the file, move it, or export to pdf or html

DO NOT add any additional packages

Save the notebook as you are working

We will only grade what is saved at the end of the exam in this exact file, and it is your responsibility to ensure the file is saved

We will not execute the notebook, so ensure all code, figures, etc. are ready as-is upon saving for submission

Ensure you edit the results in the code blocks or markup blocks indicated as we will not grade anything outside of those

You will not be judged on code quality directly, but code clarity may be required for us to ensure you understood the problem directly

If a question requires math, you can try to put latex inside of the cells but will not be judged on whether you write latex vs. math in text that doesn’t quite match latex. But it should be clear

# Packages available# DO NOT MODIFY OR ADD PACKAGESusingDistributions, Plots, LaTeXStrings, LinearAlgebra, Statistics, Random

Precompiling packages...

980.0 ms ✓ StatsAPI

1330.8 ms ✓ Statistics

1897.1 ms ✓ FillArrays

1016.4 ms ✓ Reexport

1362.9 ms ✓ DocStringExtensions

1092.3 ms ✓ PtrArrays

3866.1 ms ✓ OrderedCollections

1045.1 ms ✓ DataAPI

1754.1 ms ✓ PDMats

1282.7 ms ✓ Preferences

1036.3 ms ✓ FillArrays → FillArraysStatisticsExt

1340.3 ms ✓ Statistics → SparseArraysExt

6090.4 ms ✓ IrrationalConstants

1599.6 ms ✓ FillArrays → FillArraysSparseArraysExt

1431.6 ms ✓ AliasTables

1495.6 ms ✓ FillArrays → FillArraysPDMatsExt

3158.4 ms ✓ DataStructures

1220.9 ms ✓ JLLWrappers

1261.2 ms ✓ LogExpFunctions

4021.1 ms ✓ Missings

1288.6 ms ✓ SortingAlgorithms

1397.6 ms ✓ Rmath_jll

1467.3 ms ✓ OpenSpecFun_jll

1606.2 ms ✓ Rmath

4905.6 ms ✓ QuadGK

5811.3 ms ✓ StatsBase

4217.6 ms ✓ SpecialFunctions

922.3 ms ✓ PDMats → StatsBaseExt

1187.9 ms ✓ HypergeometricFunctions

2637.1 ms ✓ StatsFuns

4749.0 ms ✓ Distributions

31 dependencies successfully precompiled in 29 seconds. 10 already precompiled.

Precompiling packages...

913.3 ms ✓ TensorCore

928.9 ms ✓ Contour

1186.2 ms ✓ LaTeXStrings

1359.9 ms ✓ Measures

3134.9 ms ✓ Format

2188.6 ms ✓ Requires

1038.6 ms ✓ StableRNGs

5683.0 ms ✓ Grisu

8064.6 ms ✓ MacroTools

1523.4 ms ✓ URIs

1056.3 ms ✓ SimpleBufferStream

1379.1 ms ✓ TranscodingStreams

4374.6 ms ✓ Unzip

1020.0 ms ✓ DelimitedFiles

1017.9 ms ✓ BitFlags

3515.0 ms ✓ NaNMath

2347.6 ms ✓ ConcurrentUtilities

1210.7 ms ✓ LoggingExtras

1385.1 ms ✓ PrecompileTools

4121.7 ms ✓ StructUtils

1011.9 ms ✓ ExceptionUnwrapping

2704.9 ms ✓ UnicodeFun

1668.6 ms ✓ Graphite2_jll

1241.4 ms ✓ Libmount_jll

1149.6 ms ✓ EpollShim_jll

1881.3 ms ✓ LLVMOpenMP_jll

10049.8 ms ✓ FixedPointNumbers

1289.2 ms ✓ Bzip2_jll

1372.0 ms ✓ Xorg_libXau_jll

1595.3 ms ✓ Xorg_libICE_jll

1623.0 ms ✓ libpng_jll

1682.9 ms ✓ libfdk_aac_jll

1268.3 ms ✓ LERC_jll

1948.2 ms ✓ LAME_jll

1517.0 ms ✓ fzf_jll

1919.5 ms ✓ JpegTurbo_jll

1659.9 ms ✓ XZ_jll

1544.8 ms ✓ Ogg_jll

1368.2 ms ✓ mtdev_jll

1883.6 ms ✓ Xorg_libXdmcp_jll

1404.3 ms ✓ x265_jll

1646.6 ms ✓ x264_jll

1385.1 ms ✓ libaom_jll

1820.7 ms ✓ MbedTLS_jll

1425.1 ms ✓ Zstd_jll

1957.6 ms ✓ Expat_jll

1289.6 ms ✓ LZO_jll

1399.3 ms ✓ Opus_jll

1352.0 ms ✓ Xorg_xtrans_jll

1770.5 ms ✓ libevdev_jll

1829.2 ms ✓ Libiconv_jll

1192.1 ms ✓ Libffi_jll

1687.8 ms ✓ eudev_jll

1399.3 ms ✓ FriBidi_jll

1589.6 ms ✓ Libuuid_jll

1148.3 ms ✓ Showoff

1353.6 ms ✓ CodecZlib

4746.2 ms ✓ OpenSSL

4380.1 ms ✓ RecipesBase

1665.8 ms ✓ Pixman_jll

1826.7 ms ✓ FreeType2_jll

1482.6 ms ✓ Xorg_libSM_jll

5122.6 ms ✓ ColorTypes

1822.0 ms ✓ JLFzf

1618.4 ms ✓ libvorbis_jll

3049.7 ms ✓ Ghostscript_jll

2983.7 ms ✓ MbedTLS

4326.0 ms ✓ Xorg_libxcb_jll

1725.2 ms ✓ Libtiff_jll

1289.8 ms ✓ Dbus_jll

1764.3 ms ✓ GettextRuntime_jll

1986.1 ms ✓ Wayland_jll

1142.9 ms ✓ libinput_jll

2183.9 ms ✓ Fontconfig_jll

994.3 ms ✓ ColorTypes → StyledStringsExt

7131.3 ms ✓ ColorVectorSpace

13003.7 ms ✓ Colors

10537.8 ms ✓ Latexify

1158.2 ms ✓ Xorg_xcb_util_jll

1443.3 ms ✓ Xorg_libX11_jll

1666.0 ms ✓ Glib_jll

42836.8 ms ✓ Parsers

1774.8 ms ✓ Latexify → SparseArraysExt

1552.3 ms ✓ Xorg_xcb_util_image_jll

1994.8 ms ✓ Xorg_xcb_util_keysyms_jll

1571.8 ms ✓ Xorg_xcb_util_renderutil_jll

8960.0 ms ✓ ColorSchemes

1347.2 ms ✓ Xorg_xcb_util_wm_jll

1528.6 ms ✓ Xorg_libXrender_jll

1200.3 ms ✓ Xorg_libXext_jll

1234.1 ms ✓ Xorg_libXfixes_jll

1842.0 ms ✓ Xorg_libxkbfile_jll

1807.6 ms ✓ Xorg_xcb_util_cursor_jll

12502.3 ms ✓ JSON

1732.9 ms ✓ Xorg_libXinerama_jll

1782.6 ms ✓ Xorg_libXrandr_jll

2267.9 ms ✓ Libglvnd_jll

2064.3 ms ✓ Cairo_jll

1066.0 ms ✓ Xorg_libXcursor_jll

1768.2 ms ✓ Xorg_libXi_jll

1897.9 ms ✓ Xorg_xkbcomp_jll

1962.7 ms ✓ HarfBuzz_jll

1529.7 ms ✓ Xorg_xkeyboard_config_jll

1496.2 ms ✓ libass_jll

2040.7 ms ✓ Pango_jll

30642.1 ms ✓ PlotUtils

1804.7 ms ✓ xkbcommon_jll

2310.1 ms ✓ FFMPEG_jll

56360.7 ms ✓ HTTP

1820.2 ms ✓ Vulkan_Loader_jll

7445.4 ms ✓ PlotThemes

1636.5 ms ✓ libdecor_jll

1561.3 ms ✓ FFMPEG

2866.5 ms ✓ Qt6Base_jll

2094.5 ms ✓ GLFW_jll

1654.2 ms ✓ Qt6ShaderTools_jll

2060.1 ms ✓ GR_jll

12913.7 ms ✓ RecipesPipeline

3407.6 ms ✓ Qt6Declarative_jll

769.1 ms ✓ Qt6Wayland_jll

5191.7 ms ✓ GR

82652.3 ms ✓ Plots

122 dependencies successfully precompiled in 231 seconds. 55 already precompiled.

Precompiling packages...

696.4 ms ✓ ColorVectorSpace → SpecialFunctionsExt

1 dependency successfully precompiled in 1 seconds. 20 already precompiled.

Precompiling packages...

1261.6 ms ✓ QuartoNotebookWorkerJSONExt (serial)

1 dependency successfully precompiled in 1 seconds

Precompiling packages...

2616.8 ms ✓ QuartoNotebookWorkerPlotsExt (serial)

1 dependency successfully precompiled in 3 seconds

Precompiling packages...

1013.5 ms ✓ QuartoNotebookWorkerLaTeXStringsExt (serial)

1 dependency successfully precompiled in 1 seconds

Take the following functions from our previous lectures

# DO NOT MODIFYfunctionlorenz(v) # assumed sorted vector S =cumsum(v) # cumulative sums: [v[1], v[1] + v[2], ... ] F = (1:length(v)) /length(v) L = S ./ S[end]return (; F, L) # returns named tupleend# Assumes that v is sorted!gini(v) = (2*sum(i * y for (i,y) inenumerate(v))/sum(v)- (length(v) +1))/length(v)functionsimple_regression(x, y) x_bar =mean(x) y_bar =mean(y) a =sum((x .- x_bar).*(y .- y_bar)) /sum((x .- x_bar).^2) b = y_bar - a * x_barreturn (;a, b)end

simple_regression (generic function with 1 method)

Short Question 1

With a CDF of a distribution \(F(x)\) with an accompanying counter-cdf \(1-F(x)\), what is the definition of a power-law tail? For a stochastic process \(X_t\), what features of that stochastic process might lead to a power-law tail in the stationary distribution?

Answer:

(double click to edit your answer)

Short Question 2

If you are trying to understand wealth inequality, what features of the distribution are ideal to examine using (a) Lorenz Curves; (b) Gini Coefficients; and (c) Power Law Tails

Answer:

(double click to edit your answer)

Short Question 3

If I calculate a log-log plot of a distribution to examine whether it has heavy tails, what should I plot for the x-axis and y-axis? If I did a linear regression and found that the slope was -2, would that necessarily say that the distribution was a power-law distribution? Why or why not?

Answer:

(double click to edit your answer)

Short Question 4

If a log-log plot showed a slope of -1.5 with a clear linear relationship in the right tail, what is the implied power-law exponent? What does this tell us about moments of the underlying distribution?

Answer:

(double click to edit your answer)

Short Question 5

Compare stochastic processes:

\(X_{t+1} = a_{t+1} X_t + b\)

\(X_{t+1} = X_t + a_{t+1} + b\)

where in both cases \(a_{t+1}\) are IID shocks. Which stochastic process would you expect may have power-law tails in their stationary distribution, and why? What if \(b = 0\) in both cases? Provide intuition for the differences.

Answer:

(double click to edit your answer)

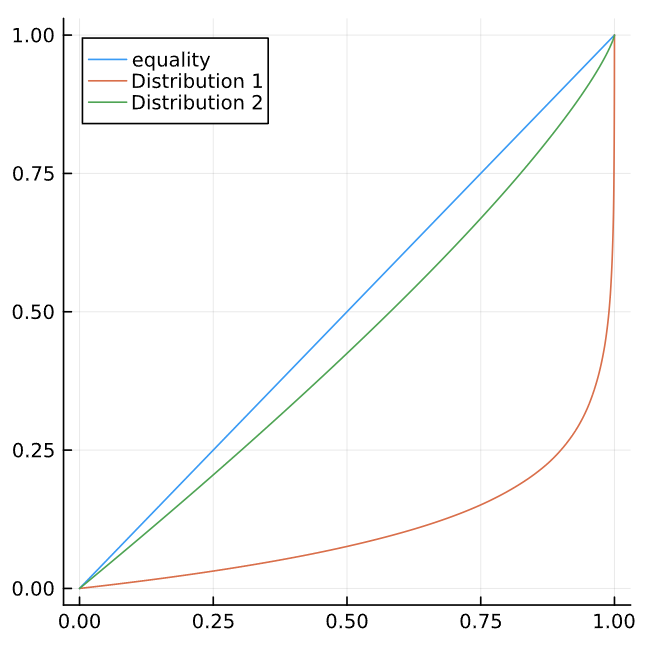

Short Question 6

Take the following figure showing the Lorenz Curves for data from two different distributions. What can you infer about the inequality in the two distributions? Roughly what would you expect the Gini coefficients to be for the two distributions?

Answer:

(double click to edit your answer)

Short Question 7

Given a mapping \(F : \mathbb{R}^N \to \mathbb{R}^N\) what is the definition of a fixed point \(x^*\) of this mapping? Does it always exist? If it exists, is it unique?

Answer:

(double click to edit your answer)

Short Question 8

Explain the importance of the fixed factor of production, land, in the Malthusian growth model

Answer:

(double click to edit your answer)

Short Question 9

An asset pays off a deterministic stream of income, \(\{y_{t+j}\}_{j=0}^{\infty}\), and a risk-neutral agent prices this using a discount factor \(0 < \beta < 1\). The PDV of the income is then \(p_t = \sum_{j = 0}^{\infty}\beta^j y_{t+j}\) The agent prices this asset using the recursive formulation

\[

p_t = y_t + \beta p_{t+1}

\]

Briefly interpret this recursive equation from the agent’s perspective.

Answer:

(double click to edit your answer)

Short Question 10

What is a state space model? Explain what type of problem a Kalman Filter solves. What are the key assumptions on the stochastic processes, priors, etc. that make it applicable?

Answer:

(double click to edit your answer)

Question 0

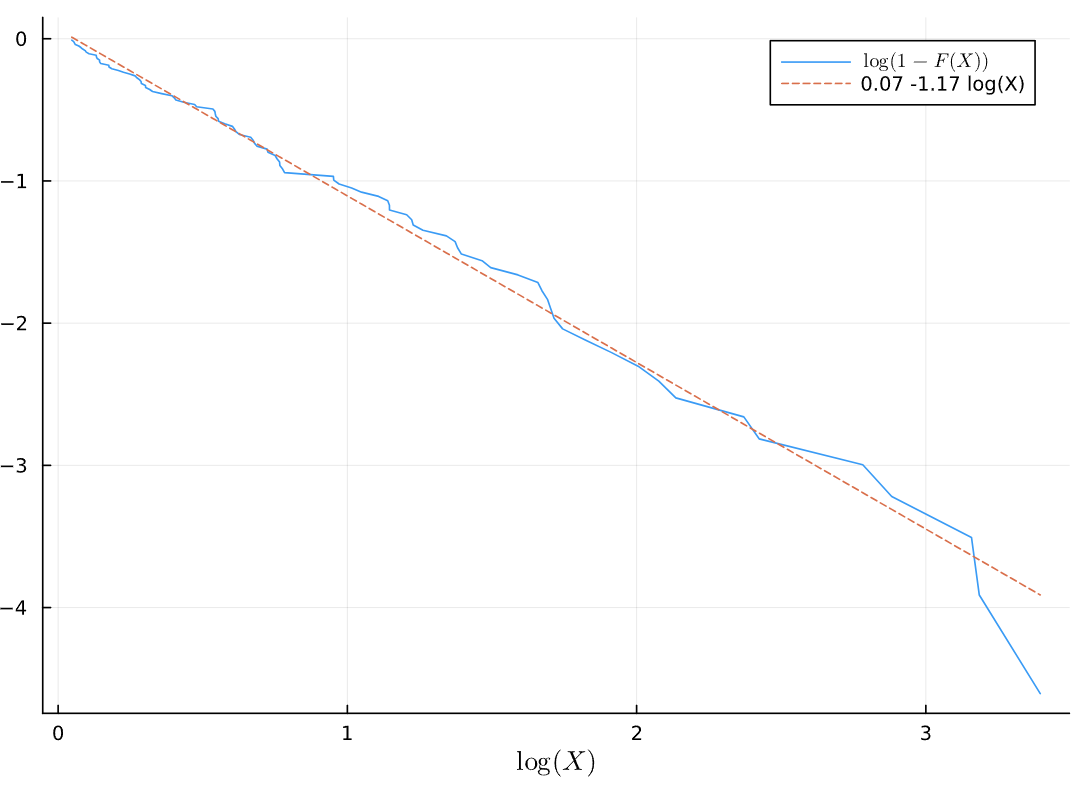

Consider for some \(X_t \sim F\) IID draws from a distribution the log-log plot using the empirical CDF. The dotted line plots the linear regression with this data, with the intercept and slope shown on the legend.

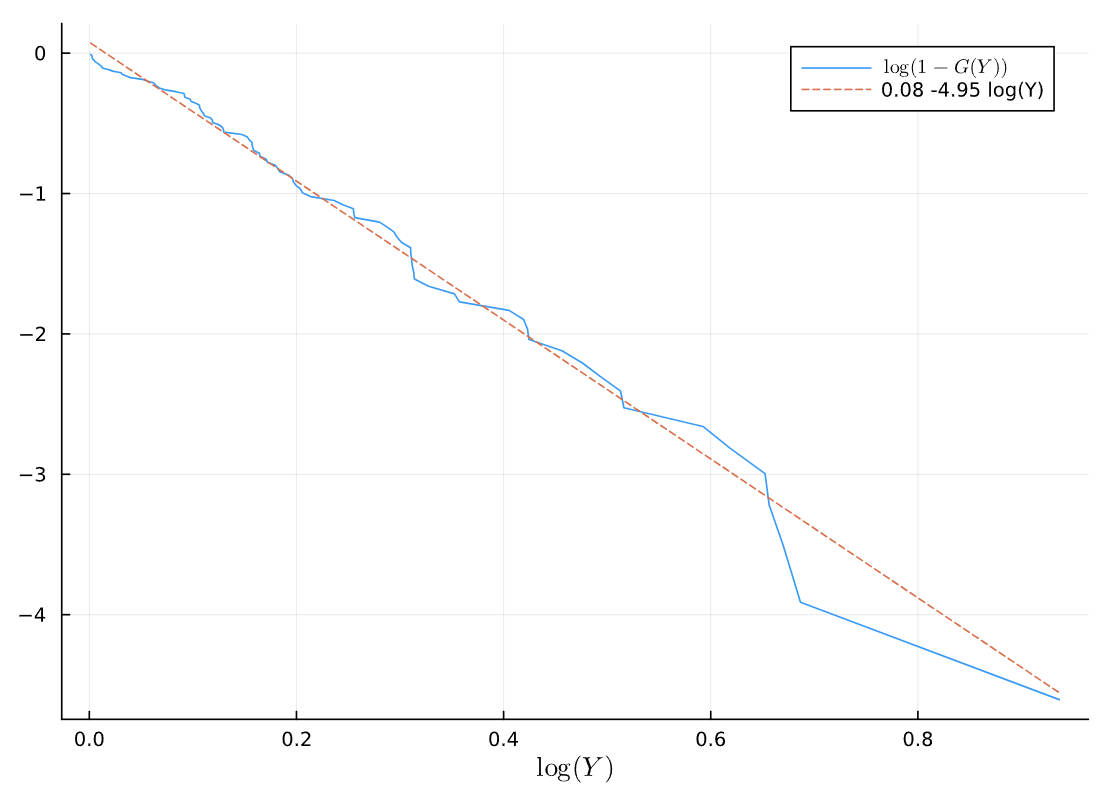

Consider the log-log plot of 100 IID draws from a different distribution \(Y_t \sim F\).

Compare the \(X_t\) and \(Y_t\) log-log plots. What can you infer about these distributions?

Answer:

(double click to edit your answer)

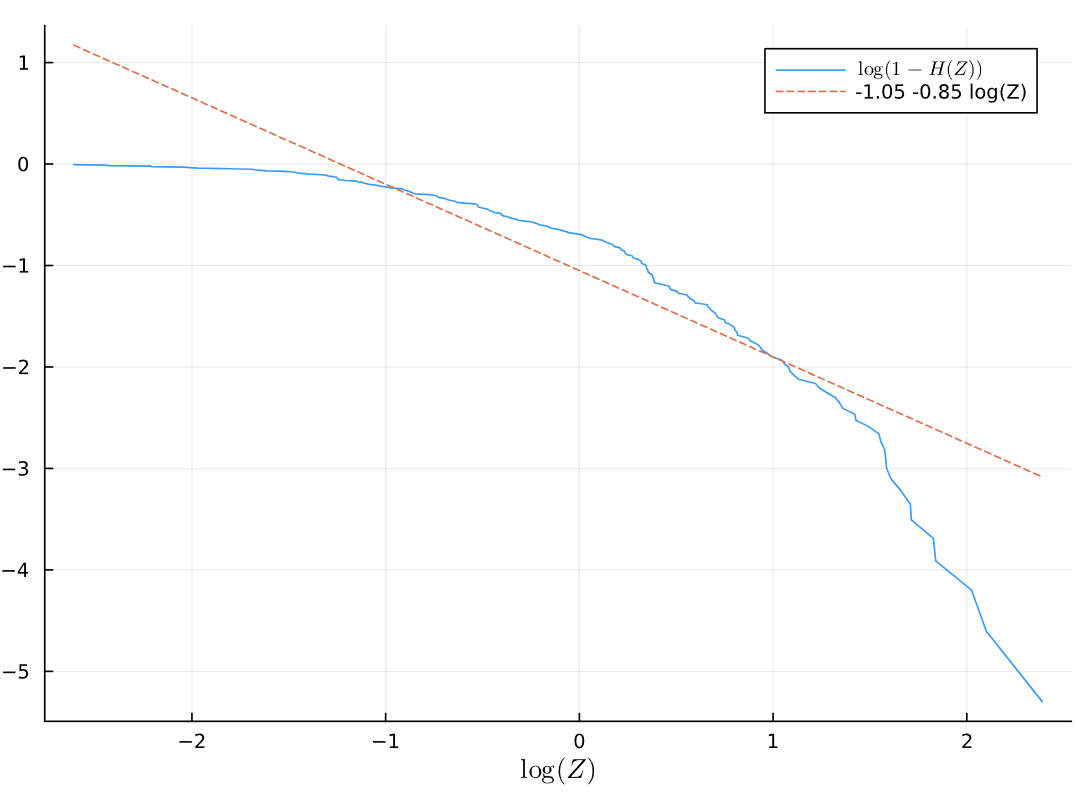

Now consider the log-log plot of draws from a third distribution \(Z_t \sim F\)

The log-log plot of the \(Z_t\) draws

What can you infer about this distribution compared to the other two?

Answer:

(double click to edit your answer)

Question 1

Following the notes on AR(1) processes rather than plotting the distribution as normal instead lets see what the stationary distribution looks like with simulation.

Part (a)

From \(X_0 = 1.0\) simulate up to \(T=2000\) using the process

\[

X_t = a X_{t-1} + b + c W_t

\]

Where \(a=0.98, b=0.1, c=0.02\).

T =2000X_0 =1.0a =0.98b =0.1c =0.02# Add code here

0.02

Part (b)

On the same graph plot the histogram of those simulated values (i.e., \(\{X_0, \ldots X_T\}\)) then plot the density of the stationary distribution calculated in closed form in those notes (i.e. create a normal distribution with \(\mu^* = b/(1-a)\) and \(v^* = c^2/(1 - a^2)\)

Hint: histogram(X, normed=true) normalizes the empirical draws so they are a proper PMF.

# Add code here

Part (c)

Now, do the same plot using the 10th to 500th observations (i.e., \(\{X_{10}, \ldots X_{500}\}\))

# Add code here

And then a separate plot using the rest

# Add code here

Compare how these line up? Explain why each is better or worse?

Answer:

(double click to edit your answer)

Part (d)

Change the c parameter to be 0.2.

Now repeat the display of the two histograms (1) split of the 10th to 500th ; and (2) the remainder

T =2000X_0 =1.0a =0.98b =0.1c =0.2# Add code here, creating new cells as required

0.2

Compare this to part (c)? Have the results changed and if so, then why?

Answer:

(double click to edit your answer)

Question 2

In this problem we will examine wealth dynamics for a simpler setup. Log income, \(\log y_t\) follows an AR(1) process,

where \(\epsilon_{1,t+1} \sim N(0,1)\) and \(\epsilon_{2,t+1} \sim N(0,1)\) are IID shocks.

As in the wealth dynamics problem from before, the evolution of wealth is given by

\[

w_{t+1} = R_{t+1}s(w_t) + y_{t+1}

\]

where \(s(w_t)\) is the exogenously given savings function from before,

\[

s(w) = s_0 w \cdot \mathbb 1\{w \geq \hat w\} = \begin{cases} s_0 w & w \geq \hat{w}\\

0 & w < \hat{w}

\end{cases}

\]

For a constant \(s_0 \in (0,1)\) which is savings rate and \(\hat{w}\geq 0\) is a minimum wealth threshold below which they do not save and instead consume all of their income (since \(w_{t+1} = y_{t+1}\) in that case).

Take the following simpler structure for holding the parameters of the model

functionsimple_wealth_dynamics_model(; w_hat=1.0, # savings parameter s_0=0.75, # savings parameter mu_y=0.1, # labor income parameter sigma_y=0.1, # labor income parameter rho_y=0.9, # labor income parameter mu_r=0.0, # rate of return parameter sigma_r=0.2, # rate of return parameter )return (;w_hat, s_0, mu_y, sigma_y, rho_y, mu_r, sigma_r)end

simple_wealth_dynamics_model (generic function with 1 method)

and a modified version of the simulate_panel function

functionsimulate_panel(N, T, p; y_0 = p.mu_y/(1-p.rho_y), w_0 = p.mu_y/(1-p.rho_y))# Setup initial conditions w = w_0 *ones(N) # start at same w_0 logy =log.(y_0 *ones(N)) # start at same y_0 logR =zeros(N) # not used in this exact example, but could be generalized# Preallocate next period states and R intermediates w_p =similar(w) logR_p =similar(w) logy_p =similar(w) # Temporary used in calculations savings_proportion =similar(w) # include constant and R_{t+1}for t in1:T R_shock =randn(N) y_shock =randn(N)@inboundsfor i in1:N logy_p[i] = p.mu_y + p.rho_y*logy[i] + p.sigma_y*y_shock[i] logR_p[i] = p.mu_r + p.sigma_r*R_shock[i] # no autocorrelation but could reference logR[i] savings_proportion[i] = (w[i] >= p.w_hat) ? p.s_0 *exp(logR_p[i]) :0.0 w_p[i] = savings_proportion[i]*w[i] +exp(logy_p[i])end# Step forward w .= w_p logy .= logy_p logR .= logR_pendsort!(w) # sorts the wealth so we can calculate gini/lorenz F, L =lorenz(w)return (;w, y =exp.(logy_p), F, L, gini =gini(w))end

simulate_panel (generic function with 1 method)

The following code shows a basic simulation,

p =simple_wealth_dynamics_model()# Or simple_wealth_dynamics_model(;w_hat = 2.0) to swap out a single parameter, etc.N =10_000T =200w_0 =10.0res =simulate_panel(N, T, p; w_0) # uses the default y_0 but overrides the w_0 default@show res.gini, mean(res.w), mean(res.y); # show some of the results

Using the above code and default parameter values, simulate the model to see the difference in the gini coefficients where you change the variance on the returns sigma_r 10 points between 0.0 to 0.3.

Using your simulations, plot the gini coefficient as a function of sigma_r and comment on the results.

# Modify/add code here, creating new cells as requiredsigma_r_values =range(0.0, 0.3, 10)N =10_000T =200# simple_wealth_dynamics_model(;sigma_r = sigma_r_values[1]) # etc. to create modified modelsres =simulate_panel(N, T, simple_wealth_dynamics_model(;sigma_r = sigma_r_values[end])) # for example, this swaps the sigma_r with the last value in the range@show res.gini;

res.gini = 0.23641318881795942

Can you provide a brief interpretation of the results?

Answer:

(double click to edit your answer)

Part (b)

Now, take the same model and lets shut off all variation on the income process to leave it as a fixed value so \(y_{t+1} = y_t\) by setting sigma_y = 0, rho_y = 1, mu_y = 0 and then initializing all of the agents with the y_0 = 5.0 and w_0 = 2.0 Calculate the gini coefficient for the same range of sigma_r values as above and plot the results.

# Modify/add code here, creating new cells as requiredp =simple_wealth_dynamics_model(;sigma_y =0.0, rho_y =1.0, mu_y =0.0)N =10_000T =1000y_0 =5.0w_0 =2.0# res = simulate_panel(N, T, p; y_0, w_0) # adapt this, passing in the y_0 and w_0

2.0

Can you provide a brief interpretation of the results?

Answer:

(double click to edit your answer)

Question 3

A risk-neutral investor with discount factor \(\beta\) values a firm. The firm’s dividends (profits) each period are revenue minus operating costs: \(d_t = r_t - c_t\).

Both revenue and costs follow AR(1) processes driven by a single common macroeconomic shock \(w_{t+1} \sim \mathcal{N}(0,1)\):

Define a state vector \(x_t\) and write down matrices \(A\), \(C\), and \(G\) such that the system can be written in LSS form:

\[

x_{t+1} = A x_t + C w_{t+1}, \quad d_t = G x_t

\]

Hint: you will need a constant in the state vector to handle the intercepts \(\mu_r\) and \(\mu_c\).

Answer:

(double click to edit your answer)

Part (b)

Using the LSS form from part (a), compute the expected present discounted value of dividends using the closed-form formula from the formula sheet:

\[

p_0 = G (I - \beta A)^{-1} x_0

\]

# Construct the matrices A, C, G and the initial state x_0# Then compute the EPDV using the formula above# Add code here

Part (c)

Verify your closed-form answer by simulation. Simulate N = 5000 paths for T = 500 periods of the two AR(1) processes, compute dividends \(d_t = r_t - c_t\), discount them, and average across paths.

N =5000T =500# For each path:# 1. Simulate r_t and c_t for T periods using the AR(1) equations# 2. Compute d_t = r_t - c_t for each period# 3. Compute the discounted sum: sum_{t=0}^{T-1} beta^t * d_t# Average the discounted sums across all N paths# Add code here

500

Does your simulation match the closed-form answer? What are the sources of any small discrepancy?

Additionally, try changing sigma_r or sigma_c and recomputing the closed-form price. Does the price change? Why or why not?

Answer:

(double click to edit your answer)

Part (d)

Investigate how the firm’s value depends on revenue persistence. Vary rho_r from 0.0 to 0.95 over 10 points, compute the EPDV for each value, and plot the result.

rho_r_values =range(0.0, 0.95, 10)# For each rho_r value, construct A and compute the EPDV using the closed-form formula# Plot rho_r_values vs. the EPDV values# Add code here

0.0:0.10555555555555556:0.95

Provide a brief interpretation: why does higher revenue persistence increase the firm’s value? Hint: what happens to the long-run mean of revenue \(\mu_r/(1-\rho_r)\) as \(\rho_r\) increases?

Answer:

(double click to edit your answer)

Formulas

Use the following formulas as needed. Formulas are intentionally provided without complete definitions of each variable or conditions on convergence, which you should study using your notes.

YOU WILL NOT BE EXPECTED TO USE THE MAJORITY OF THESE FORMULAS - BUT SOME MAY HELP PROVIDE INTUITION

General and Stochastic Process Formulas

Description 1

Formula 1

Description 2

Formula 2

Partial Geometric Series

\(\sum_{t=0}^T c^t = \frac{1 - c^{T+1}}{1-c}\)

Geometric Series

\(\sum_{t=0}^{\infty} c^t = \frac{1}{1 -c }\)

PDV

\(p_t = \sum_{j = 0}^{\infty}\beta^j y_{t+j}\)

Recursive Formulation of PDV

\(p_t = y_t + \beta p_{t+1}\)

Univariate Linear Difference Equation

\(x_{t+1} = a x_t + b\)

Solution

\(x_t = b \frac{1 - a^t}{1 - a} + a^t x_0\)

Linearity of Normals

\(X \sim \mathcal{N}(\mu_X, \sigma_X^2), Y \sim \mathcal{N}(\mu_Y, \sigma_Y^2)\) then \(a X + b Y \sim \mathcal{N}(a \mu_X + b \mu_Y, a^2 \sigma_X^2 + b^2 \sigma_Y^2)\)

Special Case

\(Y \sim N(\mu, \sigma^2)\) then \(Y = \mu + \sigma X\) for \(X \sim N(0,1)\)

Partial Sums \(X_1,\ldots\) IID with \(\mu \equiv \mathbb{E}(X)\)